HOW PAST RECESSIONS LEAVES CLUES FOR THE FUTURE OF THE INDUSTRIAL SECTOR

- Colliers | Columbus

- Apr 30, 2020

- 3 min read

Written by: Amanda Ortiz

Amanda Ortiz is the Director, National Industrial Research on the National Marketing & Research team at Colliers. Based in Chicago, Amanda partners with national and local teams to deliver market intelligence initiatives and provide direction to drive national competitive advantage through research strategy, development and analytics. Keep reading to get Amanda’s take on the future of the industrial sector, and check out her post on Colliers Knowledge Leader here.

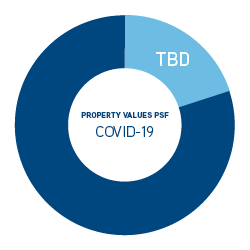

With the emergence of COVID-19, the world has entered a new down cycle. This will undoubtedly send ripples throughout the commercial real estate sector in the near term — but just how might the industrial sector fare in the aftermath of COVID-19? How much could property values and rental averages fall? Let’s look to the past for some guidance on the future.

IMPACT ON INDUSTRIAL SALES

The industrial sector has consistently proven to weather economic storms in a more favorable way compared to other property types, and this cycle remains no different. While COVID-19 has already upended markets and sent shock waves throughout the economy, the capital markets are well-positioned to answer these macroeconomic shifts. Although retail, travel and hospitality sectors have been the hardest hit thus far, data centers and industrial space are expected to sustain activity. One of the drivers of declining values appears to be the density of interaction within an asset class as retail, hospitality and even office sectors often require people in close proximity.

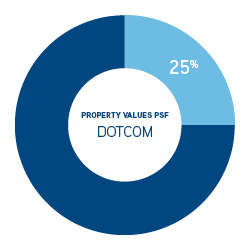

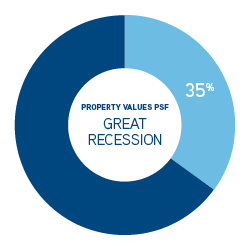

On average, industrial sale prices per square foot dropped 30% during the previous two economic downturns — the dotcom bust in the early 2000s and the Great Recession that began in 2008. COVID-19 is the third major event to rock our economy in the last 20 years and it remains to be seen what toll the current pandemic will bring. Economists have updated their initial v-shaped recovery outlook to a more conservative u-shaped recovery where a prolonged period of restoration is predicted. However, some economists are predicting a w-shaped recovery where we appear to recover, suffer another short-lived shock and then continue recovering. The United States, however, remains a haven for foreign investment and transaction velocity remains active, though slightly cooled, in 2020.

NET ASKING RATES A BRIGHT SPOT

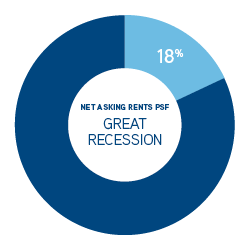

The good news for industrial owners is that net asking rents should fare much better than property values. Prior to the onset of the COVID-19 pandemic, the U.S. economy enjoyed historic economic expansion and rent growth. In fact, rental values grew 7.5% on average annually. Following the dotcom bust, industrial rents fell a mere 5% peak-to-trough as the office sector was largely affected. Peak-to-trough following the Great Recession that began in 2008 experienced a sharper decline, falling 18% — not nearly as low as sales prices following the dotcom bust or the Great Recession that fell 25% and 35%, respectively.

Occupiers of industrial space are certainly feeling the pressure of the COVID-19 crisis as requests for rent relief increase week to week. Landlord sentiment tends to be sympathetic and landlords are lowering rents in exchange for an extended lease commitment, in some cases, due to the ongoing uncertainty. Other tenants, like e-commerce suppliers, grocery and food-related users, or occupiers in other industries related to the essential workforce that are seeking to expand operations could find opportunity to lock in favorable lease terms with lower taking rents.

ADAPTABILITY IS KEY

The recent supply chain disruptions caused by the COVID-19 pandemic should cause companies to retool their existing playbooks, but the shock to industrial property values and asking rental rates are expected to be minimal. After all, industrial space could emerge from this crisis as the darling of commercial space as the need for safety stock — the counter to just-in-time (JIT) inventory strategies — becomes increasingly clear. Moreover, the demand shift to e-commerce for grocery and other consumer products should sustain industrial use, as traditional retail use declines.

The full depth of COVID-19 remains unknown, yet the demand for warehouse and distribution space should offset a rise in vacancy from occupiers unable to alter their productions. Some apparel production has shifted to sewing masks, and parts manufacturers have shifted to producing ventilator parts to aid in the production of personal protective equipment. Companies able to adapt to the current market conditions with more flexible terms and the capabilities to shift production stand to weather this storm largely unscathed.

Comments